]]>

Category Archives: Economics

Are Shareholders Obsolete?

In his January 2, 2015 Wall Street Journal essay, columnist Holman Jenkins makes a compelling case for the principle of shareholder value maximization by noting that owners seeking to maximize the value of their businesses end up doing a pretty decent job of satisfying customer and employees along the way. Think of this essay as a 2015 sequel to Milton Friedman’s famous New York Times Magazine essay (published September 13, 1970) entitled “The Social Responsibility of Business is to Increase its Profits” (see http://bit.ly/Social_Responsibility_of_Business for Friedman’s essay; Thomas Coleman provides important context in his recent (2013) essay about Friedman entitled “Corporate Social Responsibility: Friedman’s View @ http://bfi.uchicago.edu/feature-story/corporate-social-responsibilty-friedmans-view)…

What’s the “future” for price at the pump?

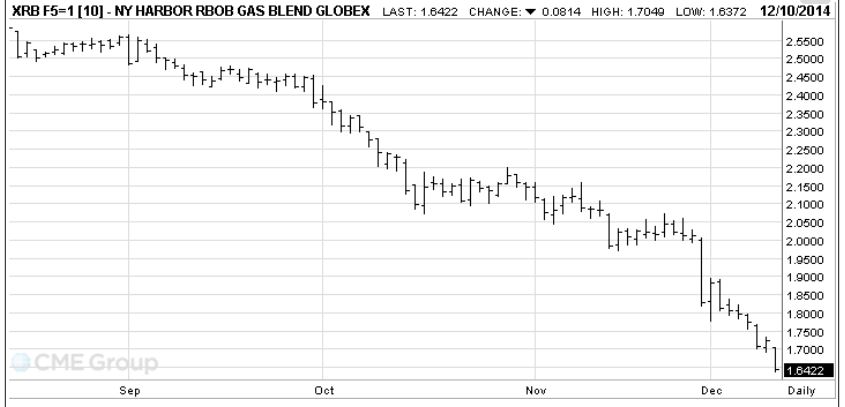

Lately, futures prices for crude oil and refined products such as gasoline and heating oil have been in a free-fall. For example, the January 2015 futures contract for “RBOB Gasoline” is trading at the equivalent of around $1.64 per gallon. As shown in the following graph, this represents a price drop of roughly 85-90 cents per gallon since September:

AAA reports that today’s national average is $2.639 and could fall to $2.50 within the next couple of weeks. Nationally, the average markup from the near term futures contract price to prices at the pump has averaged 62 cents per gallon since January 2000 (which is when AAA began tracking this information). Therefore, if futures prices hold at (or fall further from) current levels it seems quite likely that the price at the pump may be headed even lower.

What's the "future" for price at the pump?

RBOB Gasoline” is trading at the equivalent of around $1.64 per gallon. As shown in the following graph, this represents a price drop of roughly 85-90 cents per gallon since September:

AAA reports that today’s national average is $2.639 and could fall to $2.50 within the next couple of weeks. Nationally, the average markup from the near term futures contract price to prices at the pump has averaged 62 cents per gallon since January 2000 (which is when AAA began tracking this information). Therefore, if futures prices hold at (or fall further from) current levels it seems quite likely that the price at the pump may be headed even lower.]]>

Media Bias, Echo Chambers, and the Future of Democracy

This 1 hour long presentation by University of Chicago economist Matthew Gentzkow is well worth watching; Professor Gentzkow explores the implications of new media technologies for the health of American democracy.

Terrorism risk insurance

Clearly insurance is an enabling technology; without insurance many if not most large-scale commercial activities would grind to a halt. In a Business Week article entitled “The Unexpected Threat to Super Bowl XLIX“, Wharton professors Howard Kunreuther and Erwann Michel-Kerjan point out that that if Congress decides not to renew the Terrorism Risk Insurance Act (TRIA) (set to expire on Dec. 31), there is a chance that the Super Bowl might not be played. Will Warren Buffet step in as an insurer of last resort if TRIA is not reauthorized? Also, Gordon Woo raises some excellent points about possible private sector alternatives to TRIA in his blog posting entitled “RMS and the FIFA World Cup: Insuring Against Terrorism“.

On Australia’s minimum wage policy

In today’s daily USPS junk mail delivery, I was deluged (as is everyone these days) by a pile of political flyers. One of the flyers in particular caught my eye – it was entitled “Common Sense MMXIV” (why the Roman numerals? But I digress).

One of the supposed “common sense” proposals listed on this flyer was to “…. enact, as Australia has, a $20/hr. minimum wage”. Since I was not aware that Australia had a $20/hr. minimum wage, I googled this topic and found that in fact Australia does not have a $20/hr. minimum wage (source: http://www.wageindicator.org/main/salary/minimum-wage/australia). What Australia does have is a 16.87AUD/hour minimum which translates (at the current exchange rate) into 14.84USD/hour (AUD and USD are acronyms respectively for “Australian Dollar” and “US Dollar”). Furthermore, there are all sorts of caveats that apply; for example, there’s a schedule of minimum wages (expressed as a percentage of the 16.87AUD/hour baseline) based upon the age of the worker:

| <16 years: 36.8% | AUD6.21 | USD5.46 |

| 16 years: 47.3% | AUD7.98 | USD7.02 |

| 17 years: 57.8% | AUD9.75 | USD8.58 |

| 18 years: 68.3% | AUD11.52 | USD10.13 |

| 19 years: 82.5% | AUD13.92 | USD12.24 |

| 20 years: 97.7% | AUD16.48 | USD14.49 |

For more on the economics of the minimum wage, I recommend reading the attached article by David Neumark; Dr. Neumark is an economics professor and director of the Center for Economics and Public Policy at the University of California, Irvine.

On Australia's minimum wage policy

does not have a $20/hr. minimum wage (source: http://www.wageindicator.org/main/salary/minimum-wage/australia). What Australia does have is a 16.87AUD/hour minimum which translates (at the current exchange rate) into 14.84USD/hour (AUD and USD are acronyms respectively for “Australian Dollar” and “US Dollar”). Furthermore, there are all sorts of caveats that apply; for example, there’s a schedule of minimum wages (expressed as a percentage of the 16.87AUD/hour baseline) based upon the age of the worker:

| <16 years: 36.8% | AUD6.21 | USD5.46 |

| 16 years: 47.3% | AUD7.98 | USD7.02 |

| 17 years: 57.8% | AUD9.75 | USD8.58 |

| 18 years: 68.3% | AUD11.52 | USD10.13 |

| 19 years: 82.5% | AUD13.92 | USD12.24 |

| 20 years: 97.7% | AUD16.48 | USD14.49 |

This week’s Initiative on Global Markets (IGM) Economic Experts Panel statements

This week’s IGM Economic Experts Panel statements:

- Employers that discriminate in hiring will be at a competitive disadvantage, if their customers do not care about their mix of employees, compared with firms that do not discriminate.

- Rising market wages are an important reason — over and above any changes in medical technology, social norms or preferences — why family sizes have fallen over the past century in rich countries.

See http://bit.ly/Trzm4k for poll results!

Suggested books and readings on finance and risk management

In my opinion, the following 3 books are particularly worthwhile for students who are interested in learning more about finance and risk management:

- Against the Gods: The Remarkable Story of Risk, by Peter L. Bernstein.

- A Random Walk Down Wall Street: The Time-Tested Strategy for Successful Investing, by Burton G. Malkiel.

- Stocks for the Long Run : The Definitive Guide to Financial Market Returns and Long-Term Investment Strategies, by Jeremy J. Siegel.

Philosophically, these books present what I would consider to be an “orthodox” perspective; i.e., they fit well with the so-called rational choice, efficient markets view of the world which is prevalent in most departments of finance and economics. For some “heterodox” alternatives, I like (but am nevertheless highly critical of) both of Nicholas Taleb’s books:

- Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (read this first).

- The Black Swan: The Impact of the Highly Improbable (the sequel to “Fooled by Randomness”).

Finally, I would be remiss to not also include two other favorites which are not books on finance or economics; rather they deal with the history and philosophy of applied mathematics. These books include:

- Innumeracy: Mathematical Illiteracy and Its Consequences, by John Allen Paulos.

- A Brief History of Infinity, by Brian Clegg.